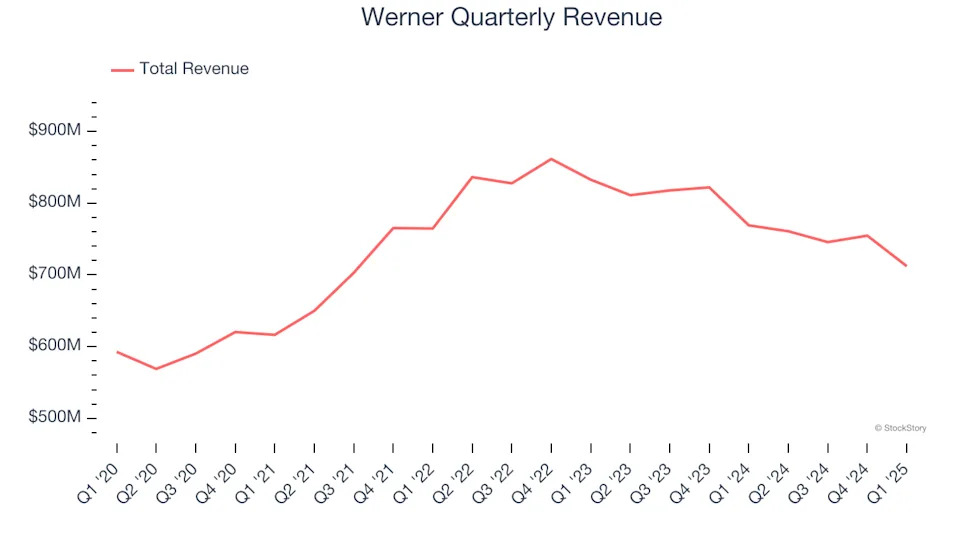

Freight delivery company Werner (NASDAQ:WERN) missed Wall Street’s revenue expectations in Q1 CY2025, with sales falling 7.4% year on year to $712.1 million. Its non-GAAP loss of $0.12 per share was significantly below analysts’ consensus estimates.

Is now the time to buy Werner? Find out in our full research report .

Werner (WERN) Q1 CY2025 Highlights:

“First quarter results were below our expectations due to elevated insurance costs, extreme weather, a smaller fleet and changes in customer activity stemming from tariff-induced uncertainty. Despite these challenges, we are seeing strength in Dedicated with a streak of wins in new fleet contracts to be implemented in the coming quarters. One-Way Truckload revenue per total mile was up modestly for the third consecutive quarter, despite weather disruptions, increased deadhead, and network inefficiencies. Logistics improved operating income and margin with ongoing focus on cost management,“ said Derek Leathers, Chairman and CEO.

Company Overview

Conducting business in over a 100 countries, Werner (NASDAQ:WERN) offers full-truckload, less-than-truckload, and intermodal delivery services.

Sales Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Regrettably, Werner’s sales grew at a sluggish 3.9% compounded annual growth rate over the last five years. This was below our standard for the industrials sector and is a rough starting point for our analysis.

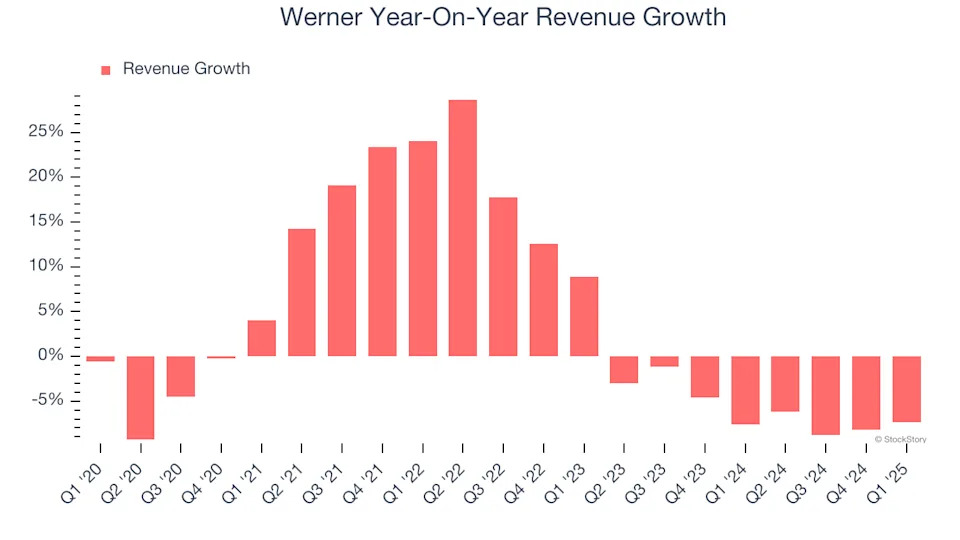

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Werner’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 5.9% annually. Werner isn’t alone in its struggles as the Ground Transportation industry experienced a cyclical downturn, with many similar businesses observing lower sales at this time.

We can better understand the company’s revenue dynamics by analyzing its most important segments, Truckload Transportation and Logistics, which are 70.5% and 27.5% of revenue. Over the last two years, Werner’s Truckload Transportation revenue (deliveries made with Werner's fleet) averaged 7.8% year-on-year declines while its Logistics revenue (brokered deliveries using third-party fleets) was flat.

This quarter, Werner missed Wall Street’s estimates and reported a rather uninspiring 7.4% year-on-year revenue decline, generating $712.1 million of revenue.

Looking ahead, sell-side analysts expect revenue to grow 5% over the next 12 months. Although this projection indicates its newer products and services will fuel better top-line performance, it is still below average for the sector.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. .

Operating Margin

Werner was profitable over the last five years but held back by its large cost base. Its average operating margin of 7.2% was weak for an industrials business. This result isn’t too surprising given its low gross margin as a starting point.

Analyzing the trend in its profitability, Werner’s operating margin decreased by 9.3 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Werner’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

This quarter, Werner’s breakeven margin was down 2.8 percentage points year on year. Conversely, its gross margin actually rose, so we can assume its recent inefficiencies were driven by increased operating expenses like marketing, R&D, and administrative overhead.

Earnings Per Share

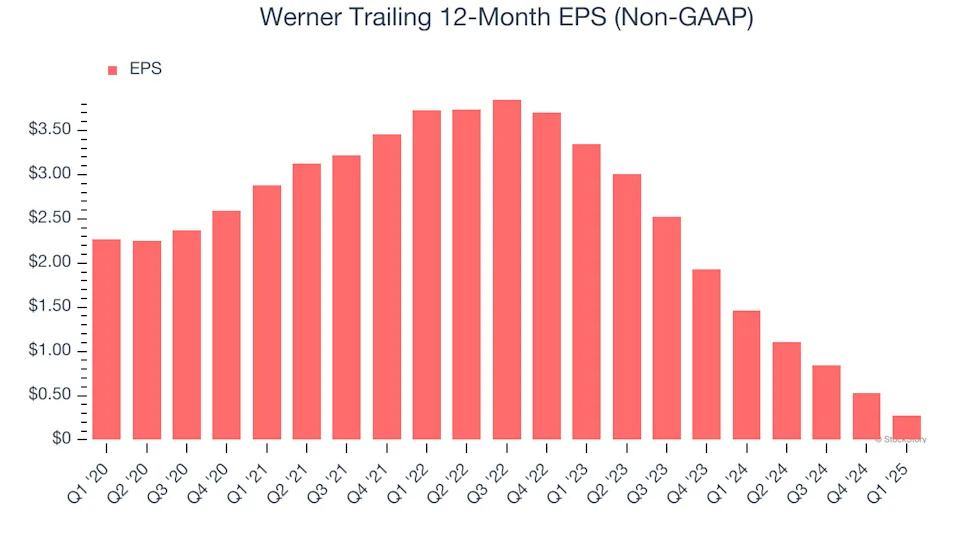

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Werner, its EPS declined by 34.4% annually over the last five years while its revenue grew by 3.9%. This tells us the company became less profitable on a per-share basis as it expanded due to non-fundamental factors such as interest expenses and taxes.

Diving into the nuances of Werner’s earnings can give us a better understanding of its performance. As we mentioned earlier, Werner’s operating margin declined by 9.3 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Werner, its two-year annual EPS declines of 71.3% show it’s continued to underperform. These results were bad no matter how you slice the data.

In Q1, Werner reported EPS at negative $0.12, down from $0.14 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects Werner’s full-year EPS of $0.28 to grow 338%.

Key Takeaways from Werner’s Q1 Results

We struggled to find many positives in these results. Its Logistics revenue missed and its revenue fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 3.8% to $26.60 immediately after reporting.

Werner underperformed this quarter, but does that create an opportunity to invest right now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free .