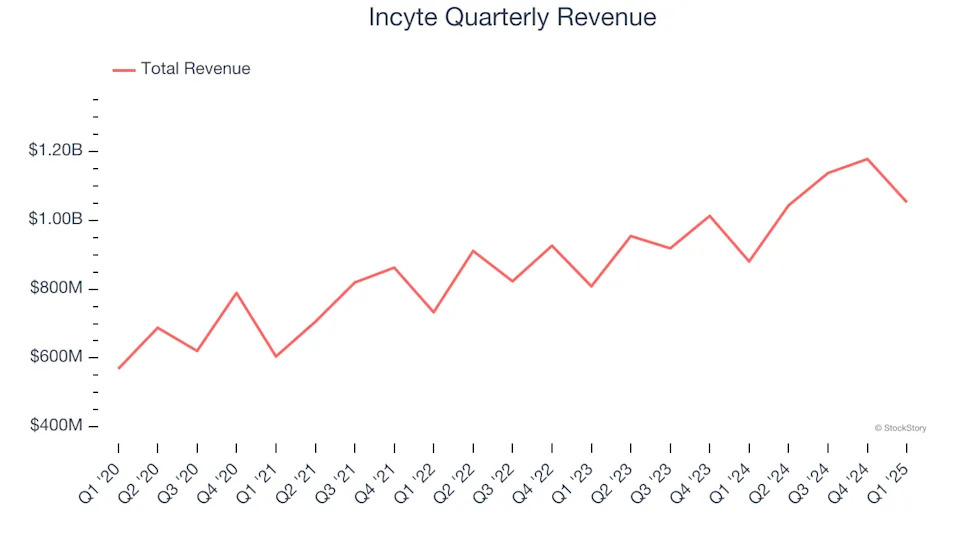

Biopharmaceutical company Incyte Corporation (NASDAQ:INCY) reported Q1 CY2025 results exceeding the market’s revenue expectations , with sales up 19.5% year on year to $1.05 billion. Its non-GAAP profit of $1.16 per share was 10.6% above analysts’ consensus estimates.

Is now the time to buy Incyte? Find out in our full research report .

Incyte (INCY) Q1 CY2025 Highlights:

"The double-digit revenue growth in the first quarter driven by the continued growth of Jakafi and Opzelura and the recent launch of Niktimvo, puts us on track to achieve our full year objectives," said Hervé Hoppenot, Chief Executive Officer, Incyte.

Company Overview

Founded in 1991 and evolving from a genomics research firm to a commercial-stage drug developer, Incyte (NASDAQ:INCY) is a biopharmaceutical company that discovers, develops, and commercializes proprietary therapeutics for cancer and inflammatory diseases.

Sales Growth

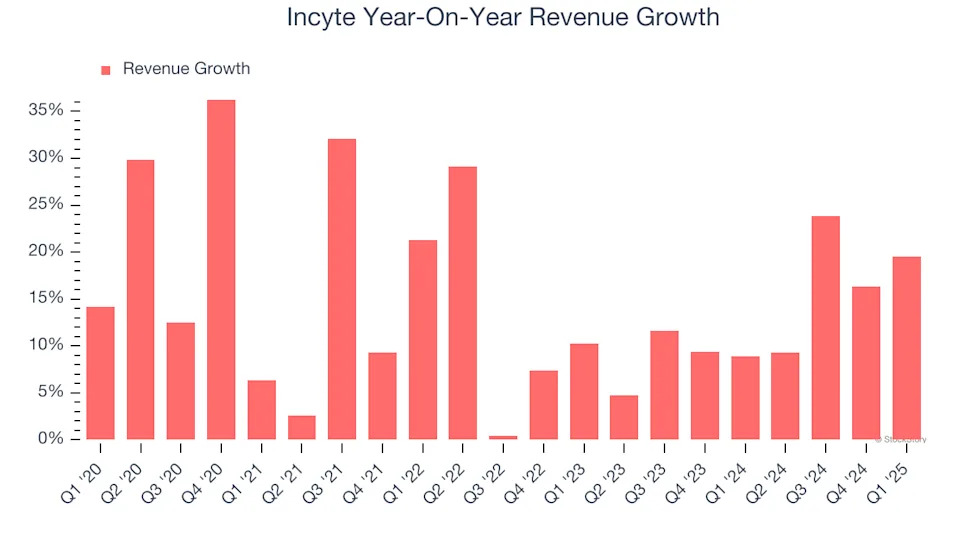

A company’s long-term sales performance can indicate its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Luckily, Incyte’s sales grew at a solid 14.6% compounded annual growth rate over the last five years. Its growth beat the average healthcare company and shows its offerings resonate with customers.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Incyte’s annualized revenue growth of 12.8% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, Incyte reported year-on-year revenue growth of 19.5%, and its $1.05 billion of revenue exceeded Wall Street’s estimates by 6.5%.

Looking ahead, sell-side analysts expect revenue to grow 8.3% over the next 12 months, a deceleration versus the last two years. Despite the slowdown, this projection is healthy and implies the market is baking in success for its products and services.

Today’s young investors likely haven’t read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next .

Operating Margin

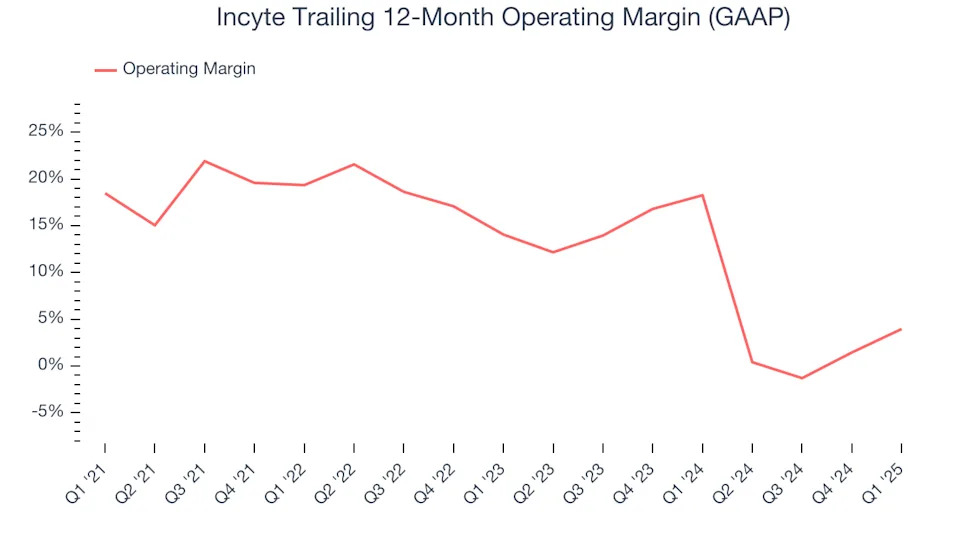

Incyte has done a decent job managing its cost base over the last five years. The company has produced an average operating margin of 14%, higher than the broader healthcare sector.

Analyzing the trend in its profitability, Incyte’s operating margin decreased by 14.5 percentage points over the last five years. The company’s two-year trajectory also shows it failed to get its profitability back to the peak as its margin fell by 10.1 percentage points. This performance was poor no matter how you look at it - it shows its expenses were rising and it couldn’t pass those costs onto its customers.

This quarter, Incyte generated an operating profit margin of 19.5%, up 9.1 percentage points year on year. This increase was a welcome development and shows it was more efficient.

Earnings Per Share

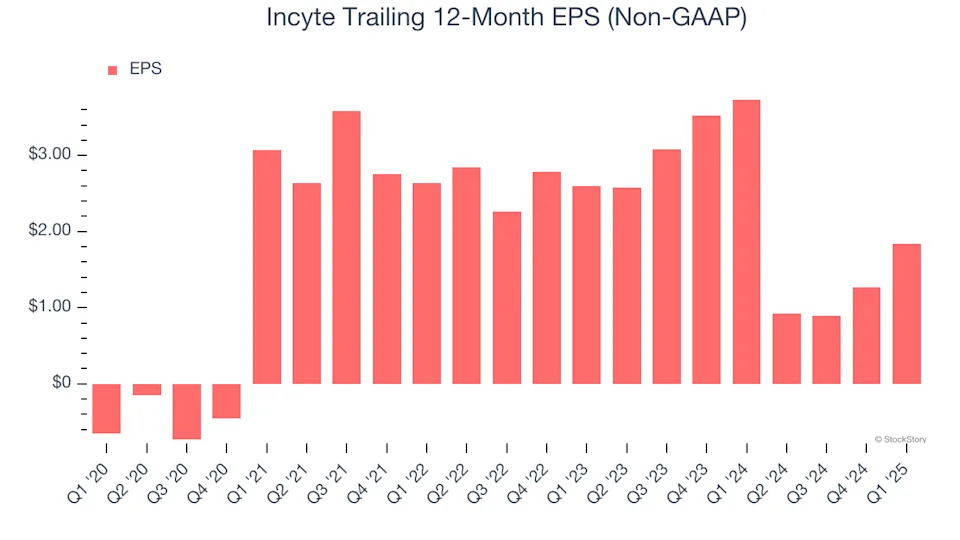

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Incyte’s full-year EPS flipped from negative to positive over the last five years. This is encouraging and shows it’s at a critical moment in its life.

In Q1, Incyte reported EPS at $1.16, up from $0.58 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Incyte’s full-year EPS of $1.84 to grow 220%.

Key Takeaways from Incyte’s Q1 Results

We were impressed by how significantly Incyte blew past analysts’ revenue expectations this quarter. We were also happy its EPS outperformed Wall Street’s estimates. Zooming out, we think this was a solid quarter. The stock remained flat at $59.52 immediately after reporting.

Indeed, Incyte had a rock-solid quarterly earnings result, but is this stock a good investment here? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free .