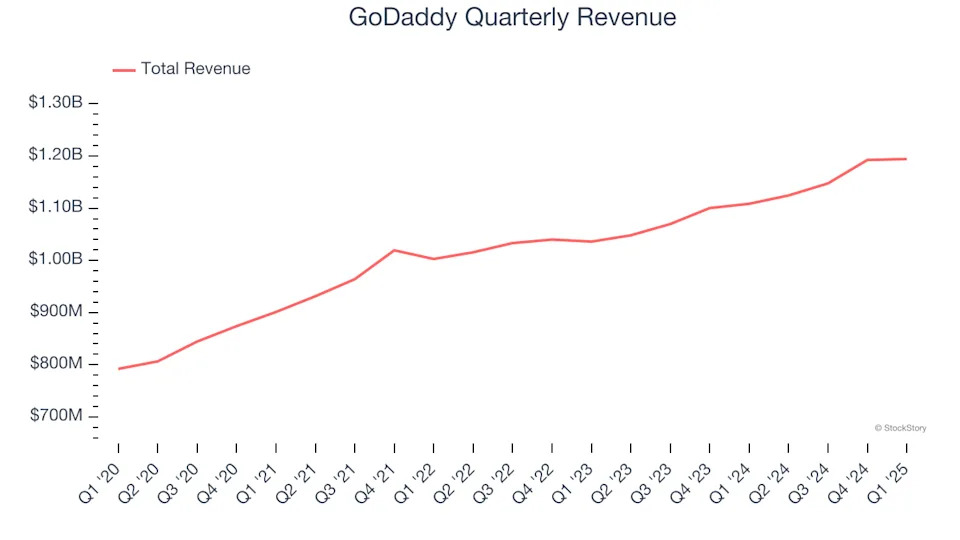

Domain registrar and web services company GoDaddy (NYSE:GDDY) reported Q1 CY2025 results exceeding the market’s revenue expectations , with sales up 7.7% year on year to $1.19 billion. The company expects next quarter’s revenue to be around $1.21 billion, close to analysts’ estimates. Its GAAP profit of $1.51 per share was 9.9% above analysts’ consensus estimates.

Is now the time to buy GoDaddy? Find out in our full research report .

GoDaddy (GDDY) Q1 CY2025 Highlights:

"GoDaddy remains well-positioned for long-term success by driving tangible, measurable outcomes that help our customers grow and thrive in any macroeconomic landscape," said GoDaddy CEO Aman Bhutani.

Company Overview

Founded by Bob Parsons after selling his first company to Intuit, GoDaddy (NYSE:GDDY) provides small and mid-sized businesses with the ability to buy a web domain and tools to create and manage a website.

Sales Growth

A company’s long-term performance is an indicator of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Regrettably, GoDaddy’s sales grew at a weak 6% compounded annual growth rate over the last three years. This was below our standard for the software sector and is a poor baseline for our analysis.

This quarter, GoDaddy reported year-on-year revenue growth of 7.7%, and its $1.19 billion of revenue exceeded Wall Street’s estimates by 0.6%. Company management is currently guiding for a 7.2% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 6.8% over the next 12 months, similar to its three-year rate. This projection is underwhelming and suggests its newer products and services will not accelerate its top-line performance yet.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. .

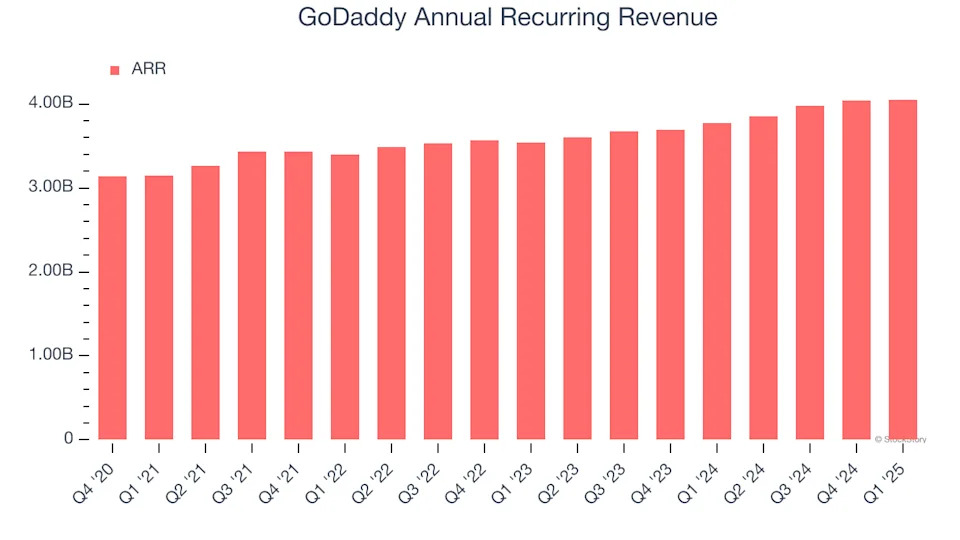

Annual Recurring Revenue

While reported revenue for a software company can include low-margin items like implementation fees, annual recurring revenue (ARR) is a sum of the next 12 months of contracted revenue purely from software subscriptions, or the high-margin, predictable revenue streams that make SaaS businesses so valuable.

GoDaddy’s ARR came in at $4.05 billion in Q1, and over the last four quarters, its growth was underwhelming as it averaged 8% year-on-year increases. This performance mirrored its total sales and suggests that increasing competition is causing challenges in securing longer-term commitments.

Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

It’s relatively expensive for GoDaddy to acquire new customers as its CAC payback period checked in at 136.7 months this quarter. The company’s slow recovery of its sales and marketing expenses indicates it operates in a highly competitive market and must invest to stand out, even if the return on that investment is low.

Key Takeaways from GoDaddy’s Q1 Results

We were impressed by how significantly GoDaddy blew past analysts’ bookings expectations this quarter. We were also happy its revenue, EPS, and EBITDA outperformed Wall Street’s estimates. On the other hand, its annual recurring revenue missed. Zooming out, we think this was a decent quarter featuring some areas of strength but also some blemishes. The market seemed to be hoping for more, and the stock traded down 6.5% to $180 immediately after reporting.

Should you buy the stock or not? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free .